Introduction:

Buying a home is a significant milestone in life, especially in the USA, where owning a home has long been part of the American dream. But before you receive the keys and begin unpacking boxes, there’s an important final step: the mortgage settlement. You may have heard it referred to as “closing” or “settlement.” Essentially, it’s the conclusion of the home-buying process. In simple terms, mortgage settlement is when all the paperwork gets signed, money is exchanged, and ownership officially transfers from the seller to you, the buyer. It’s the handshake that seals the deal after months of house hunting, negotiations, and loan approvals.

This process isn’t just a formality; it’s legally binding and involves many moving parts to ensure everything is fair. According to the Consumer Financial Protection Bureau, the closing is when you and other parties sign the necessary documents to finalize the mortgage loan and home purchase. It typically occurs at the same time as the property transfer, making it a one-stop event for most people. But how does it all work? Let’s break it down step by step, covering everything from the basics to the finer details, so you can enter your settlement feeling confident and prepared.

Understanding the Basics: What Exactly Is Mortgage Settlement?

At its core, a mortgage settlement is the legal and financial conclusion of a real estate transaction involving a mortgage. When you buy a home with a loan, this is where the lender provides the funds to pay for the property, you agree to repay the loan under specific terms, and the seller hands over the title. It’s regulated by federal laws like the Real Estate Settlement Procedures Act (RESPA), which protects consumers by requiring clear disclosures about costs and processes.

Think of it this way: You’ve found your dream home in a quiet suburb in Texas or a lively neighborhood in California. You’ve made an offer, had it accepted, and secured a mortgage pre-approval. Now, the settlement ties up all the loose ends. Without it, the deal isn’t complete; you wouldn’t own the house, and the seller wouldn’t be paid. In some cases, if issues come up during settlement, the whole transaction could fall apart, which is why preparation is essential.

It’s also important to note that “mortgage settlement” can mean something else in legal contexts, like negotiating a resolution in a mortgage dispute or foreclosure. For example, if there’s been fraud or default, parties might agree to a financial settlement to avoid court. But in everyday home buying, it mostly refers to the closing process. We will discuss those other meanings later, but for now, let’s focus on the standard home purchase situation.

The Key Players: Who’s Involved in Mortgage Settlement?

Mortgage settlement isn’t a solo effort; it involves a team of professionals working behind the scenes to ensure everything runs smoothly. Here’s a breakdown of the main participants:

- The Buyer (You): You are the star of the show. You will review and sign documents, bring any needed funds, and ask questions if something seems off.

- The Seller: They are transferring ownership. They might attend in person or sign remotely, depending on the state.

- The Lender: This is your mortgage provider, like a bank or credit union. They release the loan funds and ensure all their conditions are met.

- The Closing Agent or Escrow Officer: Often from a title company, this neutral third party handles the paperwork, collects and distributes funds, and records the deed. In some states, like California, escrow companies play a large role, while in others, like New York, attorneys might oversee it.

- Real Estate Agents: Your buyer’s agent and the seller’s agent might be there to facilitate and answer questions.

- Title Insurance Representative: They ensure the property title is free from liens or disputes.

- Attorney (If Required): In about 20 states, including Massachusetts and Georgia, buyers need a real estate attorney to review documents and represent them.

Each person’s role is critical to avoid complications. For example, the closing agent acts as the referee to make sure funds are distributed correctly, your down payment goes to the seller, loan proceeds cover the purchase price, and fees are paid to the right service providers.

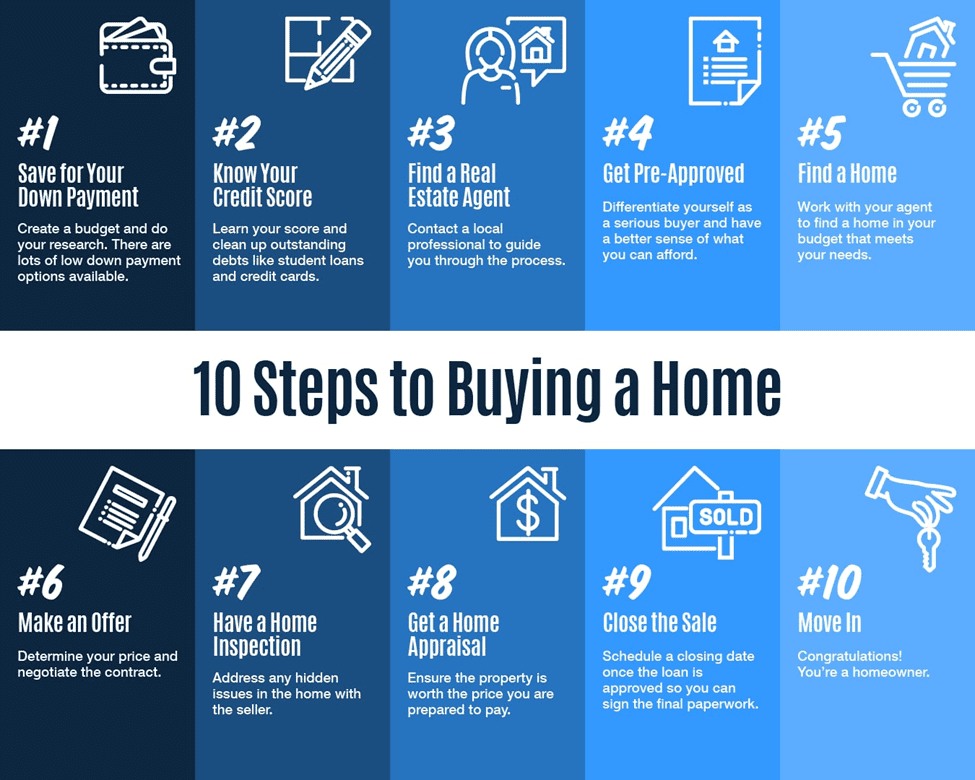

Step-by-Step: How the Mortgage Settlement Process Works

The settlement process doesn’t happen overnight. It typically starts after your loan is approved and builds up to the actual closing day. On average, it takes 30 to 45 days from loan application to closing, though this can differ based on market conditions, especially in fast-moving markets. Here’s a detailed summary:

1. Loan Approval and Scheduling:

Once your mortgage is underwritten and approved, the lender sends a “clear to close” notice. The closing agent then schedules the settlement date, usually at their office, a title company, or even remotely through e-signing in states that allow it.

2. Review the Closing Disclosure:

By law, you must receive this document at least three business days before closing. It lists all costs, loan terms, and cash needed to close. Compare it to your initial Loan Estimate to spot any discrepancies. If there are unexpected fees, address them immediately.

3. Final Walkthrough:

About 24 hours before closing, you inspect the home to ensure it’s in the agreed-upon condition, with no new damage from the seller’s move-out.

4. Closing Day Arrival:

Bring photo ID, a cashier’s check for closing costs (wire transfers are common, too), and any required documents like proof of insurance. The session can last 1-2 hours.

5. Signing Documents:

You’ll sign a stack of papers, exceeding 100 pages! Key documents include the promissory note (your promise to repay the loan), the deed of trust (which secures the lender’s interest), and the settlement statement (detailing all financial aspects).

6. Fund Disbursement:

The closing agent collects your down payment and loan funds, pays off the seller’s mortgage if necessary, and distributes fees.

7. Recording and Keys:

The deed is recorded with the local government, officially making you the owner. You receive the keys, congratulations!

This process ensures transparency and protects all parties involved. In escrow states, funds are held until everything is verified, adding an extra layer of security.

The Timeline: From Offer to Ownership

Timing is crucial in real estate. After your offer is accepted, the clock starts ticking. Most purchase contracts set a closing date 30-60 days out, allowing time for inspections, appraisals, and loan processing. Delays can occur due to appraisal issues or title problems, so it’s wise to build in some buffers.

For example, in a typical scenario: Week 1-2 for home inspection and negotiations; Week 3 for appraisal; Weeks 4-5 for underwriting; and the final week for disclosures and walkthrough. If you’re in a competitive market like Florida’s coastal areas, things might speed up, but always plan for the unexpected.

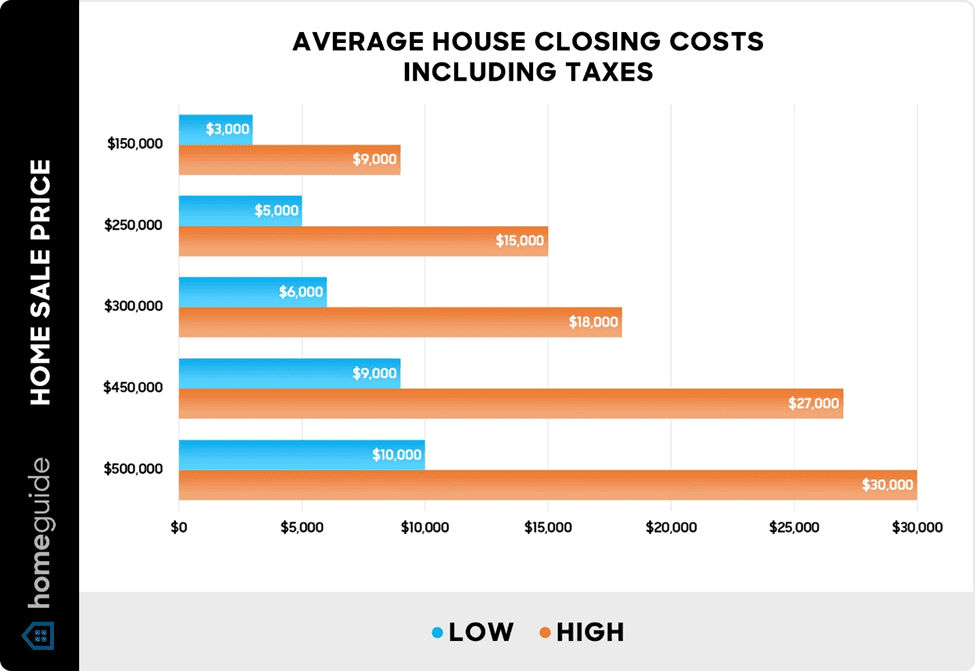

Breaking Down Closing Costs: What You’ll Pay

Closing costs are the fees and expenses beyond the home’s price, typically 2-5% of the loan amount for buyers. They can accumulate quickly; on a $300,000 home, that’s $6,000-$15,000. Here’s a breakdown:

- Lender Fees: Origination (1% of loan), appraisal ($300-500), credit report ($30-50).

- Title-Related: Title search ($200-400), title insurance ($1,000+), settlement fee ($500-1,000).

- Government Fees: Recording ($50-100), transfer taxes (vary by state, e.g., 1% in Pennsylvania).

- Prepaids: Homeowners insurance (first year), property taxes (prorated), interest (from closing to first payment).

- Other: Home inspection ($300-500, paid earlier), attorney fees (if needed, $500-1,500).

Sellers often cover some costs, like their agent’s commission (5-6% total, split). Negotiate who pays what in your contract. Shop around for services like title insurance to save money.

Essential Documents: What You’ll Sign and Why

The paperwork can feel overwhelming, but each document has a purpose. Key ones include:

- Closing Disclosure: Summarizes costs and terms.

- Promissory Note: Your IOU to the lender.

- Mortgage or Deed of Trust: Gives the lender a lien on the property.

- HUD-1 or ALTA Settlement Statement: Itemizes all transactions (HUD-1 for older loans).

- Deed: Transfers ownership.

- Affidavits: Confirm facts like no liens.

Bring copies of your ID, loan approval, and insurance binder. Review everything; mistakes can lead to issues down the line.

Common Pitfalls and How to Avoid Them

Even with preparation, things can go wrong. Title issues, like undiscovered liens, affect 25% of transactions. Low appraisals can jeopardize deals if the home value falls below the offer. Funding delays from incomplete paperwork are common as well.

To avoid these issues: Get a title search done early, double-check your finances, and keep in touch with your team. If interest rates change, consider locking them in. In the worst cases, you might walk away, but that’s rare with good professionals involved.

After Settlement: What Happens Next?

After closing, your lender manages the loan, and payments are sent there. You will receive a monthly mortgage statement. Update your utilities, change your address, and enjoy your new home! If problems arise, such as defects not caught during the inspection, you might have options through warranties.

For refinances, settlement is similar but focuses on the new loan terms without transferring the property.

Special Cases: Mortgage Settlements in Disputes

Sometimes “mortgage settlement” means resolving legal issues. In foreclosures, you might negotiate a settlement to reduce debt or avoid eviction. The 2012 National Mortgage Settlement provided relief to millions affected by robo-signing scandals, including principal reductions and cash payments. If you are facing hardship, contact your servicer for modifications.

Tips for a Smooth Mortgage Settlement

Preparation pays off. Start by improving your credit, saving for costs, and choosing trustworthy professionals. Read all documents, ask questions, and consider using a walkthrough app like HomeZada to track everything. In the 2026 market, with rising rates, compare lenders for the best deals.

Tips for a Smooth Mortgage Settlement

Preparation pays off. Start by boosting your credit, saving for costs, and choosing reliable pros. Read all the docs, ask questions, and consider a walkthrough app like HomeZada for tracking. In 2026’s market, with rising rates, shop lenders for the best deals.

In conclusion:

Navigating the Mortgage Settlement: Your Final Step to Homeownership

A mortgage settlement, often referred to as “closing,” is much more than just a formal meeting to sign a mountain of paperwork; it is the definitive moment where your vision of homeownership becomes a legal reality. Whether you are navigating the historic neighborhoods of Ohio or settling into the sun-drenched suburbs of Arizona, this final step represents the culmination of weeks of financial scrutiny and emotional investment. During this process, the property’s title is cleared, loan funds are officially disbursed, and the deed is recorded, effectively transferring the keys from the seller to you. Understanding the weight of these documents ensures that you aren’t just signing blindly, but are instead making an informed, confident commitment to your financial future and your new community.

FAQs

They’re the same thing; closing refers to signing documents while settlement emphasizes the financial exchange.

Typically, 2-5% of the home price, covering down payment and fees, minus credits.

Yes, in many states via e-closing, especially after COVID

Negotiate repairs or credits; you can delay closing if needed.

Usually, the seller pays for the owner’s policy, and the buyer pays for the lender’s.

About 1-2 hours, but plan for more time if questions come up.

You can extend the contract; costs like rate locks might increase

It’s required in some states but optional in others, although it can be helpful.

Often, yes, but sometimes they sign separately.

A neutral account that holds funds until all conditions are met.